What is the Wind Turbine Gearbox Market Overview – Definition, scope, and significance?

The Wind Turbine Gearbox Market comprises manufacturers and suppliers of gearboxes that convert low‑speed rotor movement into high‑speed electricity‑generating shaft rotation for wind turbines. Its scope covers planetary and spur gear designs for both onshore and offshore installations. Gearboxes are critical for optimizing turbine efficiency, reducing mechanical stress, and extending service life, making them a linchpin in the renewable‑energy value chain and a decisive factor in the overall cost‑competitiveness of wind power projects.

What are the main drivers, restraints, challenges, and opportunities in the Wind Turbine Gearbox Market?

Key drivers include the global push for clean energy, rising offshore wind capacity, and the need for higher‑efficiency turbines, which boost demand for robust gearboxes. Restraints stem from the growing preference for direct‑drive (gearless) turbines and supply‑chain bottlenecks. Challenges involve high reliability standards, harsh marine environments, and escalating raw‑material costs. Opportunities arise from advances in condition‑monitoring technologies, modular gearbox designs, and increasing retro‑fit projects for aging wind farms.

What growth trends are currently shaping the Wind Turbine Gearbox Market?

Current trends feature a shift toward planetary gearboxes due to their compactness and superior load distribution, alongside a resurgence of spur gear solutions for low‑cost onshore projects. Digital twins and predictive maintenance are being integrated to reduce downtime. Additionally, manufacturers are collaborating with turbine OEMs to co‑develop customized gearboxes that match larger rotor diameters and higher tip‑speed ratios, driving incremental performance gains.

How has COVID‑19 impacted the Wind Turbine Gearbox Market and what is the recovery trajectory?

The pandemic caused temporary project delays, supply‑chain disruptions, and reduced capital spending in 2020‑2021, leading to a short‑term dip in gearbox orders. However, fiscal stimulus for renewable energy, coupled with the fast‑track approval of wind projects, sparked a rapid rebound. By 2023, demand recovered to pre‑pandemic levels, and the market entered a growth phase that is projected to accelerate through 2032.

Who are the major competitors and what is the state of consolidation in the Wind Turbine Gearbox Market?

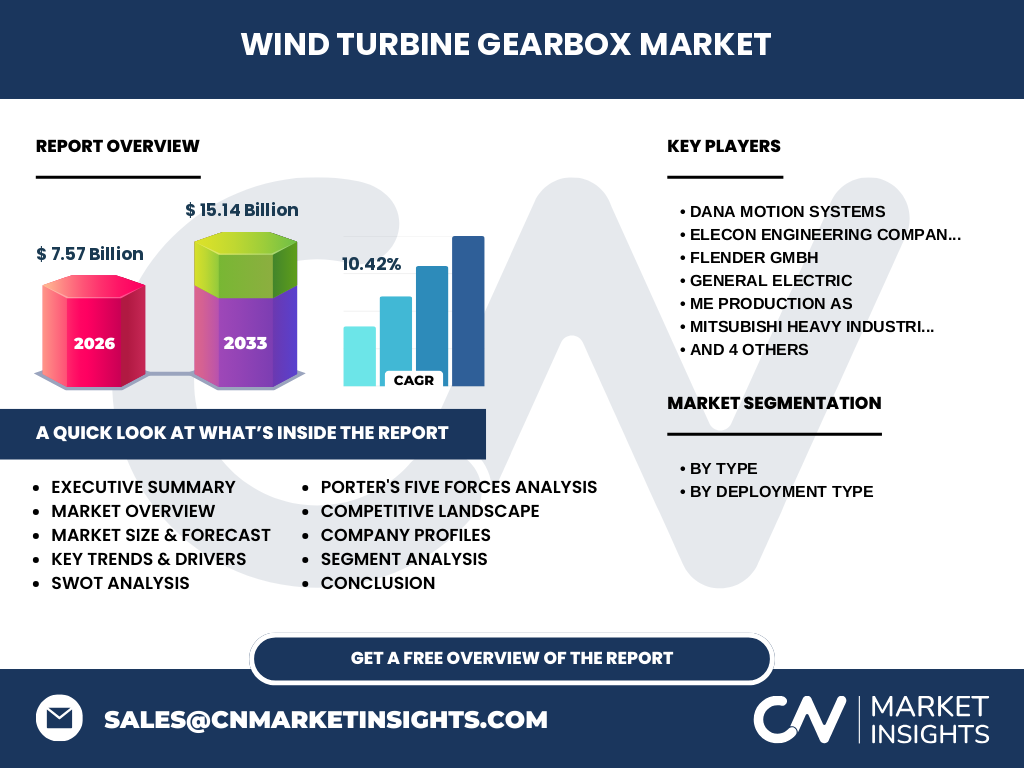

Leading competitors include Dana Motion Systems, Elecon Engineering, Flender GmbH, General Electric, ME Production AS, Mitsubishi Heavy Industries, Siemens Gamesa Renewable Energy, Stork Gears & Services BV Ltd., Vestas Wind Systems, and ZF Friedrichshafen AG. The market is moderately consolidated, with a handful of large OEMs commanding significant share, while niche players focus on specialized planetary or offshore‑grade gearboxes, fostering both competition and strategic partnerships.

What are the key findings presented in the Executive Summary?

The market is valued at USD 7.57 billion in 2026 and is projected to reach USD 15.14 billion by 2033, reflecting a robust CAGR of 10.42%. Planetary gearboxes dominate the technology mix, especially for offshore turbines, while spur gearboxes retain relevance in cost‑sensitive onshore segments. Geographic growth is strongest in Europe and Asia‑Pacific, driven by ambitious offshore targets. Digitalization and modular designs are identified as primary catalysts for the next growth cycle.

What are the forecast expectations for the Wind Turbine Gearbox Market from 2025 to 2032?

Based on the provided CAGR of 10.42%, the market is expected to expand from approximately USD 7.0 billion in 2025 to over USD 15 billion by 2032. This trajectory assumes steady offshore deployment, continued turbine up‑scaling, and incremental adoption of advanced condition‑monitoring solutions. The forecast underscores a transition toward higher‑capacity gearboxes capable of handling 10‑12 MW turbine platforms.

How is the Wind Turbine Gearbox Market sized and shared by segmentation?

By type, the market splits between planetary gearboxes—favoured for their high torque capacity and compact footprint—and spur gearboxes, which offer lower cost for smaller onshore turbines. By deployment, onshore installations account for the majority of volume due to their larger installed base, while offshore projects, though fewer in number, contribute a disproportionate share of revenue because of higher‑priced, marine‑grade gearboxes.

What is the global geographic distribution of the Wind Turbine Gearbox Market?

Europe leads in market share, propelled by extensive offshore wind programmes in the North Sea and Baltic regions. Asia‑Pacific follows, driven by rapid onshore expansion in China and India and emerging offshore projects in Japan and South Korea. North America maintains a solid foothold, primarily through onshore farms in the United States, while the Middle East and Africa present nascent yet growing opportunities linked to new renewable‑energy targets.

What are the detailed regional performance insights for the Wind Turbine Gearbox Market?

In Europe, gearbox orders are concentrated in the United Kingdom, Germany, and the Netherlands, reflecting high offshore capacity. Asian markets show strong demand for spur gearboxes in China’s vast onshore portfolio, while Japan’s offshore push drives planetary gearbox sales. The United States exhibits steady growth in onshore turbine repowering, creating retrofit gearbox demand. Emerging markets in the Middle East are beginning to source offshore‑grade gearboxes for pilot projects.

Which companies are leading in the Wind Turbine Gearbox Market and what strategies are they employing?

General Electric and Siemens Gamesa leverage vertical integration with their turbine platforms, offering bundled gearbox‑turbine solutions. ZF Friedrichshafen and Flender focus on advanced planetary designs and aftermarket service contracts. Dana Motion Systems expands through strategic acquisitions of niche gear suppliers, while Mitsubishi Heavy Industries emphasizes reliability certifications for offshore applications. Vestas and ME Production AS target cost‑efficiency for onshore projects through standardized spur gearbox lines.

How does Porter’s Five Forces framework apply to the Wind Turbine Gearbox Market?

Competitive rivalry is high due to several established OEMs and aggressive pricing. Threat of new entrants is moderate; high capital requirements and certification barriers limit newcomers. Bargaining power of buyers is strong, as turbine manufacturers can dictate specifications. Bargaining power of suppliers is moderate, with limited sources for high‑grade steels and bearings. Threat of substitutes is rising, given the growing interest in direct‑drive turbines that eliminate gearboxes.

What is the SWOT analysis for the Wind Turbine Gearbox Market?

Strengths: Essential component for most turbines, proven technology, strong OEM relationships.

Weaknesses: Susceptible to wear, high maintenance cost, competition from gearless solutions.

Opportunities: Offshore market expansion, digital monitoring, retro‑fit services.

Threats: Direct‑drive adoption, raw‑material price volatility, regulatory changes affecting certification.

How is the value chain structured in the Wind Turbine Gearbox Market?

The value chain begins with raw‑material suppliers (precision steel, bearings), proceeds to component manufacturers (gears, shafts, housing), then to gearbox assemblers who integrate and test units. After assembly, OEMs incorporate gearboxes into turbine nacelles, followed by installation firms, and finally operators who conduct O&M and end‑of‑life recycling. After‑market services such as condition monitoring and spare‑parts logistics add significant revenue streams.

What investment insights can be drawn for the Wind Turbine Gearbox Market?

Investors should prioritize companies with strong offshore portfolios and demonstrated digital‑service capabilities, as these segments command premium pricing. Capital allocation toward R&D for lightweight planetary gearboxes and predictive‑maintenance platforms can yield high returns. Partnerships with turbine OEMs and participation in government‑backed offshore projects provide stable, long‑term cash flows.

What are the concluding takeaways from the Wind Turbine Gearbox Market analysis?

The market is on a decisive growth path, underpinned by a 10.42% CAGR and a near‑doubling of revenues by 2033. Planetary gearboxes are set to dominate high‑capacity offshore projects, while spur gearboxes will retain relevance for cost‑sensitive onshore farms. Digitalization, modular designs, and strategic OEM collaborations emerge as the key levers for sustained profitability.

What research methodology was employed for this market study?

The study combined primary interviews with industry experts, OEMs, and aftermarket service providers, alongside secondary data collection from company reports, trade publications, and government databases. Quantitative analysis utilized time‑series forecasting based on the provided CAGR, while qualitative insights were derived through SWOT, Porter’s Five Forces, and value‑chain mapping.

What is the scope of this research and its limitations?

The scope covers global Wind Turbine Gearbox market size, segmentation by type and deployment, regional distribution, competitive landscape, and forward‑looking forecasts to 2033. Limitations include reliance on publicly available data and the exclusion of confidential pricing agreements, which may affect precise market‑share calculations.

Which key companies have announced recent developments in the Wind Turbine Gearbox Market?

General Electric unveiled a next‑generation planetary gearbox designed for 12 MW offshore turbines. Siemens Gamesa announced a partnership with a digital‑monitoring startup to embed sensor suites in its gearboxes. ZF Friedrichshafen introduced a modular gearbox platform aimed at simplifying offshore installation. Mitsubishi Heavy Industries reported a new manufacturing line in Japan to increase capacity for spur gearboxes targeting onshore projects. Vestas highlighted a retrofit program offering spare‑part kits for legacy turbines.